By Adam Cmejla, CFP®

Sept. 29, 2021

The decision to sell your business “baby” is one of the most important—and emotional—decisions that a practice owner will make.

Building the emotions of a practice sale into a financial equation or valuation calculator is impossible, but getting a better handle on the financial implications of selling versus staying independent can help bring clarity to part of the decision-making process.

It’s All About Cash Flow

The key practice cash-flow question is: “Do you want it now or later?” Let’s expand on this.

When a buyer is interested in purchasing a practice, they’ll calculate what they are willing to pay today for the rights to the profits of the company in the future, and compare that to the return they wish to earn on their money.

For example, let’s say that a buyer wants to earn a 15 percent return on their money a year from now, and the pre-tax profit of your practice is $400,000. This means the buyer will pay $347,826 today to earn the $400,000 in profits over the next year. This is called the discount rate. For every year that you sell early, you’re effectively selling part of those future profits “on sale” to your buyer. (1 + the discount rate and dividing that into the present value. So in my example: $400,000/1.15=$347,826).

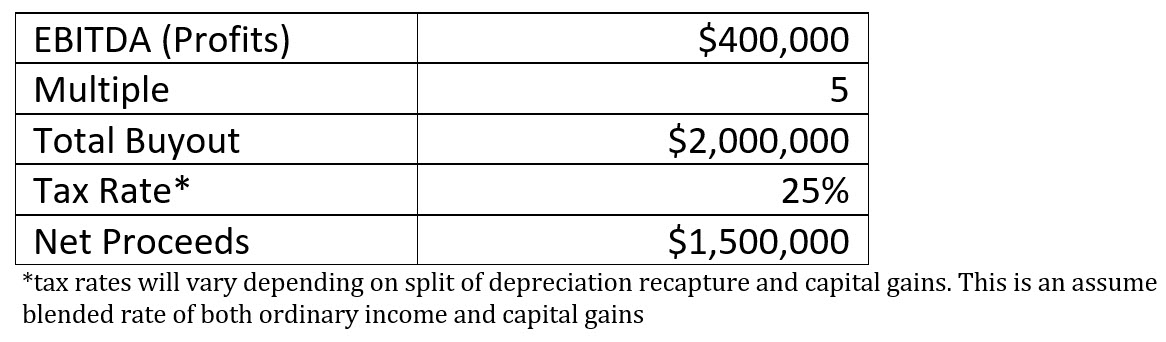

Why is this important? Remember, the number your buyer is going to offer is a combination of their discount rate (the amount of money they’ll offer upfront in exchange for your practice’s future profits) multiplied by a multiplier. Making some assumptions, let’s say a hypothetical practice sells to private equity for a 5x adjusted EBIDTA valuation that looks like this:

(Note: I’d like to clarify that your buyer is, effectively, setting their own rate of return on the money they’re investing into your business, so please don’t start comparing the aforementioned return to the return that you’d make in a well-diversified portfolio. If your buyers demanded/wanted a 22 percent return on their money, then their number would be $327,869.

The reason I bring all of this up is because it’s easy to look at only the surface level of the “now versus later” debate: Do I want to get a lump sum for my business now or retain the ability to collect future profits for XX years in the future?

However, the importance of understanding “XX” in my previous paragraph is part of why having a clear vision of your overall retirement and financial independence plan is so important. Let me explain why knowing this number influences both your ability to stand firm in your negotiations as a seller and have the clarity to know when you can confidently make “work optional” as a practice owner OD. In the end, it comes down to something that we repeatedly bring up with practice owners: Multiple diversified streams of income from different asset classes.

Income Statement Rich, Balance Sheet Poor

If you’ve read Robert Kiyosaki’s “Rich Dad Poor Dad” you’ll know one of the key lessons in that book is that the accumulation of assets isn’t the end goal—it’s turning those assets into an income stream.

Your practice is both an asset and an income stream. Determining which one of those is more valuable to you at this stage in your life is dependent on the rest of the planning you’ve done.

Let’s say that the practice owner in the example above has let “lifestyle creep” follow the success of their practice and, consequently, they have only accumulated $500,000 of additional assets in a variety of retirement (401(k), IRA, and Roth IRA) and brokerage accounts. Post-sale, their investment portfolio is now $2 million. If we use either the widely-used 4 percent distribution rule or a lesser-known, dynamic 5.3 percent distribution rule, this portfolio will produce pre-tax income between $80,000 and $106,000.

Compared to the pre-sale, slightly-less-after-EBITDA-adjustments profits of $400,000, this is a big income gap that will need to be made up in some manner if the OD wants to continue living their same quality of life post-sale that they were pre-sale. This may be through social security optimization strategies, rental real estate (including the building that the practice may be operating within), or other assets.

In this scenario, it may be better for the OD to do thorough planning to determine how they can (a) reduce their lifestyle expense over the next XX number of years while (b) saving as much profit from the practice for future retirement needs. The benefit of executing this strategy is that it allows them to harvest the cash flow from the practice now while keeping the enterprise value of the practice for a sale in the future, hopefully when their personal balance sheet is healthier.

Income Statement, Balance Sheet Rich

Admittedly, this is the best-case scenario for an OD to be in, and one which gives them all the power at the negotiating table. When an OD is confident about not only the value of diversified assets they have, but also how those assets can be converted into an income stream for retirement, they can come to the negotiating table prepared with “their number” that will work for their plan. It’s now up to the buyer (whether that’s PE or another OD) to determine if that number fits their own financial plan.

Other Articles to Explore

Continuing with the example above, let’s say that the OD hasn’t saved an additional $500,000, but instead, has prudently and consistently invested over their career, building a portfolio of $2 million. If their monthly expenses are such that, combined with other income streams, a $3.5 million portfolio ($2 million + $1.5 million practice sale) is enough to provide for the quality of life in their retirement, they are in full control of the who, when and, how much, factors in any practice negotiating. Having this confidence and clarity can make managing the other emotions I mentioned earlier a lot easier.

Prudently Plan Instead of Rapidly Reacting

It’s often said that history doesn’t repeat itself, but it often rhymes. The closing of this article is going to sound similar to other articles I’ve gratefully penned for this audience: Ending up in the second example doesn’t happen by chance. It happens through prudence, stewardship and intention. If you’re nearing the decision point within your practice, tomorrow’s going to come whether you start planning or not. Why not engage in the process and take as much control of the future outcome as possible?

Adam Cmejla, CFP® is a CERTIFIED FINANCIAL PLANNERTM Practitioner and Founder of Integrated Planning & Wealth Management, LLC, an independent financial planning & investment management firm focused on working with optometrists to help them reach their full potential and achieve clarity and confidence in all aspects of life. For a number of free resources, visit https://integratedpwm.com/ebooks/ and check out the “20/20 Money Podcast” to get more tips on making educated and informed financial and business decisions.

Adam Cmejla, CFP® is a CERTIFIED FINANCIAL PLANNERTM Practitioner and Founder of Integrated Planning & Wealth Management, LLC, an independent financial planning & investment management firm focused on working with optometrists to help them reach their full potential and achieve clarity and confidence in all aspects of life. For a number of free resources, visit https://integratedpwm.com/ebooks/ and check out the “20/20 Money Podcast” to get more tips on making educated and informed financial and business decisions.