Sponsored Content

By Bob Schultz

CEO, Vision One Credit Union

Which could put more money in your pocket, a Private-to-Private or Private Equity (PE) Sale? The answer may surprise you.

Nov. 3, 2021

Too often practice sellers only compare the “Stated Sale Price” when reviewing offers. How likely are sellers to receive the Stated Sale Price? This article will provide you a tool to analyze a broader range of factors to compare the “Total Expected Value” of Private-to-Private optometric practice sales and Private Equity sales.

The examples expressed herein do not depict any specific PE company sales terms. Private sale examples are based on standard industry practice metrics and values for well-performing practices. The methodology is a means for you to make an objective comparison. Your outcome will vary based on your due diligence and input.

For PE sales, Total Expected Value includes the funding of the Net Sale Price plus the likely realization of any Holdback. For Private sales, Total Expected Value is the Stated Sale Price plus any earnings differential between holding the practice and a reduced wage that may be paid by PE for an employment term. This comparison should be based on the contractual terms, requirements and differences between the two sale types.

On the surface, PE sales appear more lucrative as they are based on Stated Sale Price (Table 1). Is it truly more lucrative to sell to PE? You need to analyze the factors. A $1,000,000 revenue practice is used as an example because you can scale it up or down to fit your practice size. If you have $2 million in revenue, just multiply the calculations in this example by two. Likewise, for $3 million gross collected revenue, multiply by three or for $700,000 in revenue, multiply by .7.

In this illustration, values are stated as a percentage of revenues for comparison purposes, although it is not a proper means of valuation.

Vision One Credit Union is the only financial institution solely dedicated to independent optometric practices. It is all we do. Founded in 1951, by ODs for ODs, we are not for profit with an all OD, all volunteer Board.

Achieving optometric practice growth and value requires continuous investment and a long-term banking relationship. We take the time to know you, your goals and capabilities. Vision One Credit Union, because your team matters. You will appreciate the difference.

Our full banking services include:

Practice Transitions – Practice purchase, startup, partner buy in, exit strategy development (with affiliates) and execution.

Practice Growth – Purchase or startup additional location(s), relocation, remodel, equipment loans.

Wealth Building – Commercial real estate, location consolidation (rollups). A full range of deposit services including interest checking, financial planning (with affiliate).

Time Savings and Convenience – We offer full-scope financial services needed by an optometric practice. As the only banking organization asked to present Management CE at major optometric events, we know the business of optometry.

(800) 327-2628

Monday through Friday

7:30 a.m. to 4:30 p.m. (Pacific Time)

www.VisionOne.org

PE Sale – Assigning Probabilities to Determine Total Expected Value

Valuing a Holdback

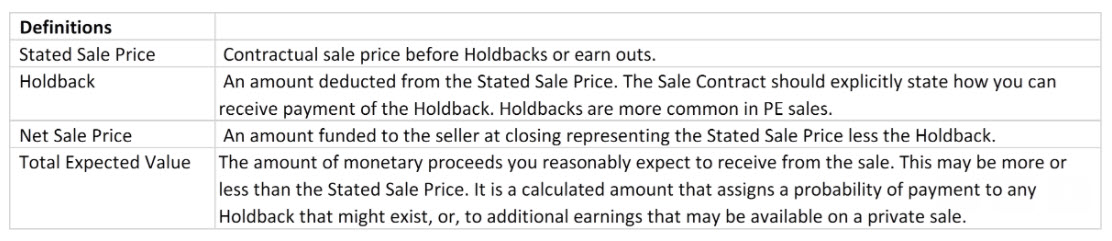

Will the PE sale require a Holdback of a portion of the Stated Sale Price which will reduce your sale proceeds upon closing? What percentage of the sale price will be held back 20%, 30%, 50%? The Net Sale Price only is paid at closing (see Table 2 for calculation).

If a Holdback is used, what are the requirements for you to receive payment of the Holdback? Do you have to achieve practice performance targets? Is there a requirement that the PE company must be sold, perhaps at a certain price over the cost of their acquisitions? Are you contractually required to work in and manage the practice? Is there one or multiple requirements?

What is the probability of being paid all or a portion of the Holdback? This is an essential question to answer if you are going to assess the Total Expected Value of a PE sale. Do you have control over the means to satisfy the Holdback requirements? Do you have visibility into the condition of the company or know the market conditions required to achieve a needed sale price of the company?

- If you have a contractual provision to work in and manage the practice

- Does the term of your employment meet your retirement timing?

- What will your ongoing compensation be for your time worked?

- Will the compensation be adequate to support your needs and lifestyle?

- How does the compensation compare to your current compensation as an owner? Calculate the difference.

- If there is a performance requirement for your practice

- Are the requirements clearly defined?

- Can you reasonably meet the requirements?

- Will you have control over the means of practice production such as staffing, equipment, frames, lens and lab choices to meet the performance requirements?

- If the PE company must be sold for you to receive payment of your Holdback

- Do you know the sale price required?

- How is the sale price determined? Does it include the cost of PE company practice acquisitions, repayment of borrowed capital, profits for the funding source and the PE company owners and the sum of all Holdbacks?

- What is the priority of payout when a PE company sells? In other words, who gets paid first, the funding source, then the PE owners, then the Holdbacks?

- What is the economic impact on your Holdback if your PE company sells to another PE company and no Holdbacks are paid out?

- What is the market demand for large blocks of practices given the supply?

- What is the financial performance of the PE company? This includes the company cash flow trending and same store sales for practice locations held more than one year. It’s not good enough to say the PE company revenues are up due to new acquisitions.

If any of these requirements exist in your sale contract, and you have information and can measure these factors, then you can assess the probability of receiving your Holdback. If not, then you should use a lower probability and value of a Holdback in your Total Expected Value calculation.

Other Articles to Explore

Calculating the Net Value of the Holdback (Holdback x Probability of Payment)

For illustration purposes, we have chosen to use a 30% Holdback. Use the actual Holdback percentage quoted by PE or the prevailing Holdback percentage generally found in your market for practices with your revenue size. We used a 20% probability of receiving the Holdback based on the assumptions we made which included limited-to-no data available to us from PE companies, the unknowns of supply and demand for large practice groups and the lack of an established market. You should set your own probability based on your personal due diligence and knowledge.

Multiply the Holdback amount by the probability of payment to get the “Net Value of the Holdback.” Then calculate the Total Expected Value of the PE Sale by adding the Net Sale Price (funded at close) and the Net Value of the Holdback. See Table 2. The values used are for example purposes, your results may vary.

Private-to-Private Sale – Assigning Probabilities to Determine Total Expected Value

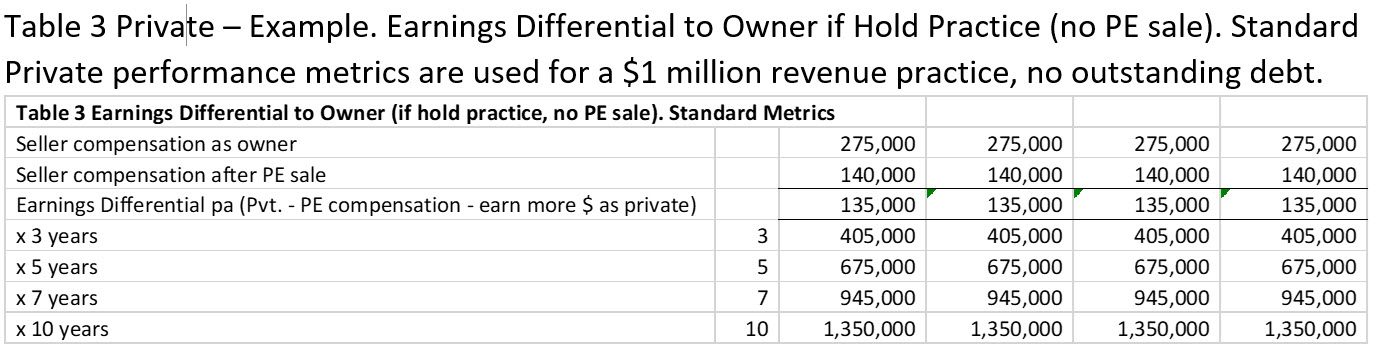

Private-to-Private sales are generally funded at one time, at closing based on a loan from a banking organization such as Vision One Credit Union. Private practice values are derived from a multiple of Free Cash Flow (also known as Ownership Premium, see article “The Only Number Needed to Determine Practice Performance” for instructions on how to calculate Ownership Premium for your practice). A practice with standard industry operating metrics should achieve a value of 73% of revenue in the current market. Practices that perform above this level can achieve higher values; lower performance produces less value. This is known as “Economic Value.” Let’s look at the value enhancements that may be available over and above the Sale Price.

Earnings Differential

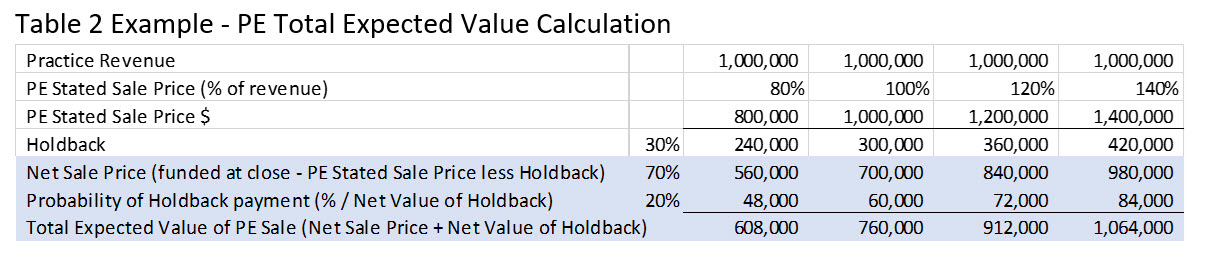

If the PE company requires a seller to stay on and manage the practice, determine what your ongoing compensation will be. Will your compensation be set to an associate wage? Practice owners generally make more than associates. The difference between your compensation now, and the PE compensation may create an earnings differential that can be valued and added to the Total Expected Value of a Private sale. You may be working either way for some defined period depending on your contract, so you should put a value on it.

For example, if a practice owner or owners are making $275,000 per year and compensation is reduced to an associate wage of $140,000 per year post sale it would result in an Earnings Differential loss of $135,000 per year (or gain if you kept the practice Private). Will you need to dip into the funds received from PE’s initial payout to make personal ends meet as opposed to putting the funds in your retirement account? Check in your area for the details of what compensation level is being offered by PE.

This example of a $135,000 Earnings Differential is used in Table 3 below. If the mandatory employment period is three years, then 3 x $135,000 per year equals $405,000 “Additional Compensation” you can earn by holding your practice and not selling to PE. If the mandatory employment period is five years, then the Additional Compensation is $675,000, etc. This should be a high-probability earn out as you remain in control of the practice as owner and an experienced manager.

Now calculate the Net Value of Additional Earnings and the Total Expected Value of a Private sale.

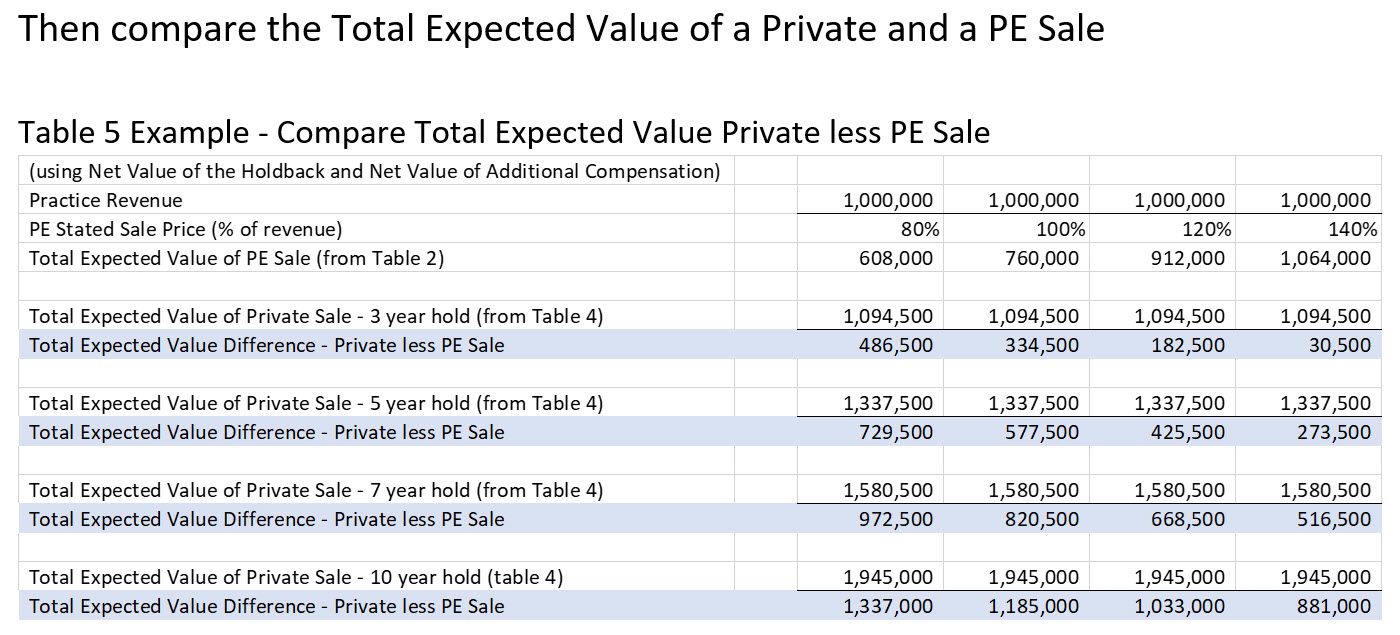

The key to this analysis is to assess the broader range of income sources and factors that impact payment to you for both sale types. The details of a PE sale matter as much or more than the Stated Sale Price. By assigning probabilities to the payouts for both Private and PE sales, you can calculate Total Expected Value. Be candid in your assessment, particularly regarding elements of payment you do and do not know or have control over. The other takeaway is the longer you hold Private, assuming standard operating margins, the more you should make. Consider these factors before you decide to exit ownership and your legacy is a commercial practice:

• Will the sale price complete your retirement fund if you do not receive your Holdback, particularly if you sell before turning 65?

• How do you feel about leaving your home market if needed to work as an associate or open another practice?

• Does the probability of additional earnings from holding your practice give you some assurance that you can make as much or more over time even if the Holdback is paid?

• How will your staff be impacted by a sale?

Try calculating Total Expected Value for your situation. Develop your own probabilities and values using the format from the tables above. If you have any questions about standard industry operating metrics or this methodology, please contact me at: BSchultz@VisionOne.org.

Since 1951 Vision One Credit Union has provided banking services exclusively to independent optometrists, helping ODs grow practices and find the best path forward. Contact us today at 916.363.4293. Because your team matters!

Bob Schultz is the CEO of Vision One Credit Union. To contact: BSchultz@visionone.org

Bob Schultz is the CEO of Vision One Credit Union. To contact: BSchultz@visionone.org