By Adam Cmejla, CFP®

Dec. 19, 2018

It’s the time of year when businesses often give to charity. Charitable giving is a good deed—and it also offers tax benefits to small businesses. Here’s how donations to charities impact the taxes you pay, and how to optimize potential savings.

New Tax Laws May Affect Tax Write-offs

As discussed in my last article, the Tax Cuts and Jobs Act passed at the end of 2017 created a myriad of new planning opportunities while also creating the need to revisit already existing strategies. Charitable giving strategies are not immune to these changes.

Many practice owners that have supported charitable and non-profit causes through their practice may be wondering if, or how, the new tax laws impact their strategy. To answer this question, we must first answer the question of whether the deduction you are claiming is actually a charitable contribution, or rather, a business expense.

Other Articles to Explore

Unless your practice is set up as a C-corporation, it will most likely be in your best interest to have contributions made to non-profits as a business expense rather than a charitable contribution/donation. To be realized as a business expense, the payment must not be classified as a charitable contribution or gift by the organization, and it must also be directly related to your business.

If the transaction (a) does not fit that criteria and (b) your business is set up as any other entity other than a C-corporation, then the contribution will be realized as a charitable contribution and the business owner may be able to deduct the contribution on their Schedule A as a part of their 1040 return. However, if they do NOT itemize their deductions, and rather claim the standard deduction, the contribution will serve no “benefit” from a tax deduction point of view.

Here are a few examples.

I’ve often seen practice owners support their local Little League baseball or softball teams. Let’s assume that one of your kids is on the team and you’ve been asked if you’d be interested in having the practice sponsor a billboard that will be hung on the outfield fence advertising your practice and showing your support.

Your sign includes the phrase “Accepting new families of patients,” or something similar. You pay $2,000 to the team, and the sign costs you another $250 to produce. You can deduct the total of $2,250 as a business expense because the goal of the sign is to serve as advertising for your practice.

However, a strategy that might be misunderstood as a business expense could be the following: A local homeless shelter asks your practice to sponsor the annual fundraising gala by purchasing a table for 10. You and your spouse invite eight of your friends to join you for the evening.

The total contribution is $2,000, and the centerpiece of your table has a sign with the verbiage “ABC Family Eyecare proudly supports XYZ Homeless Shelters.” Then, after the event, you receive a letter from the homeless organization showing the itemized breakdown of your contribution: $2,000 contribution – $1,000 value of goods/services received (dinner & drinks for your table) = $1,000 charitable contribution.

In this situation, you will likely have to count this contribution as a charitable donation on your personal tax return and itemize it on your 1040 Schedule A. Whether you will actually be able to “use” the deduction will be predicated upon whether your itemized deductions are larger than the new standard deduction in 2018 and beyond ($12,000 single, $24,000 MFJ).

For practice owners, the significant increase in the standard deduction, as well as changes and limitations to how itemized deductions are tabulated, leads into charitable planning strategies that should be evaluated on the personal side.

As a reminder, everything that’s being discussed are for illustrative purposes only and should not be viewed as individual advice. As with all planning, consult your qualified CFP® Professional and/or tax advisors if you have questions about how any of these strategies may apply to your circumstances.

Charitable Lumping

Those used to giving a certain dollar amount to their local charities on an annual basis should consider charitable lumping strategies. This involves deferring your contributions and “banking” them for a number of years to make one larger donation in the near future rather than consecutive smaller donations.

Example: You routinely give $5,000 per year to a local charity and usually make the donation around the end of the year. While meeting with your CPA and CFP® you realize that, because of the new SALT (state and local taxes) deduction limitation, you will not be able to itemize your deductions this year (an all-too-common occurrence for those living in high income tax rate states).

Editor’s Note: A comprehensive explanation of the current law capping deductions for SALT (state and local taxes) at $10,000, is provided by the Tax Policy Center.

Rather than making the charitable donation, you withhold the donation this year, park the funds in a high-yield online savings account (assume a 2 percent interest rate), make another $5,000 contribution into the savings account at EOY 2019, and in 2020 donate the total amount ($15,000 of principle plus earned interest) to the charity.

This strategy has its obvious benefits and drawbacks. The benefits are being able to claim a higher deduction in the year that you donate (assuming the above variables stay constant). The drawback is that the charity that you support has been deprived of funds that it may be counting on as part of its operating budget. Having served on non-profit boards and budget committees in the past, some organizations don’t work with a high degree of margin, and if many donors took this approach, it could have realistic hindrances to the work that the organization can perform.

If you are considering this strategy, it would be wise to be transparent with the charity and let them know of your intentions. Once you have all the information, you can make an informed decision whether this makes sense for you—financially and otherwise.

Donor Advised Funds

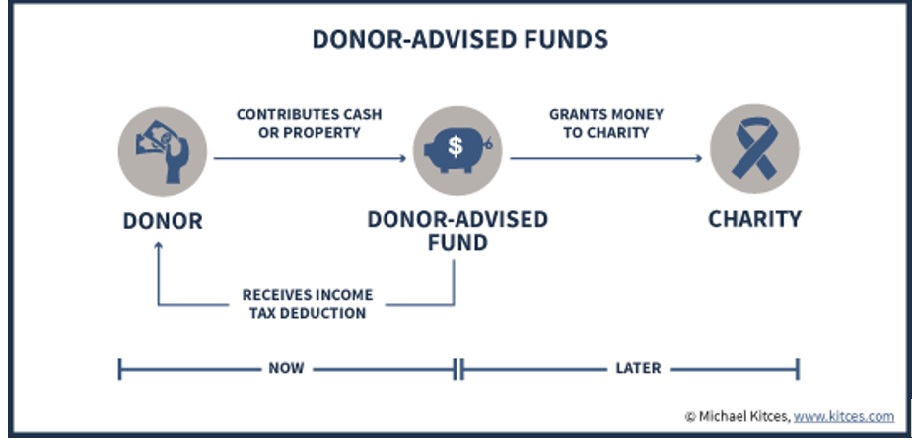

The use of Donor Advised Funds (DAFs) have increased and become an integral planning piece for those that are charitably inclined.

The following image, courtesy of Michael Kitces, illustrates how a DAF works:

This strategy can give the donor “the best of both worlds,” and has a number of benefits. First, donations can be made to the DAF in one year, but the donations to the charity can be spread out over a number of years. Second, DAFs can allow for anonymous donations. Thirdly, for larger donations, they can be much more cost-effective than setting up a family or private foundation.

Another benefit that’s worth mentioning can be very specific to private practice owners that are close to, or having their, liquidity event (selling their practice). In the year you sell your practice and realize a significant windfall of income, it may make tax- and financial-planning sense to make a large contribution to a DAF all in one year.

The benefit of this strategy is being able to claim a much higher charitable deduction in one year, but then being in control of how much, to whom, and in what years, distributions from the fund are made to various charitable organizations. Because you don’t have to name the charities at the time of the donation, this can be a very useful and powerful planning tool, especially in light of new tax law changes.

Adam Cmejla, CFP® is a CERTIFIED FINANCIAL PLANNER TM Practitioner and Founder of Integrated Planning & Wealth Management, LLC, an independent financial planning & investment management firm focused on working with optometrists to help them reach their full potential and achieve clarity and confidence in all aspects of life—personally, professionally, and financially. For a free copy of his “Top Five Tips to Financial Freedom” visit https://bit.ly/2Mo3NV8.

Adam Cmejla, CFP® is a CERTIFIED FINANCIAL PLANNER TM Practitioner and Founder of Integrated Planning & Wealth Management, LLC, an independent financial planning & investment management firm focused on working with optometrists to help them reach their full potential and achieve clarity and confidence in all aspects of life—personally, professionally, and financially. For a free copy of his “Top Five Tips to Financial Freedom” visit https://bit.ly/2Mo3NV8.