By Mark Wright, OD, FCOVD,

and Carole Burns, OD, FCOVD

July 1, 2020

The Small Business Administration (SBA) updated its forgiveness guidelines for small business owners who received loans through the Paycheck Protection Program (PPP).i

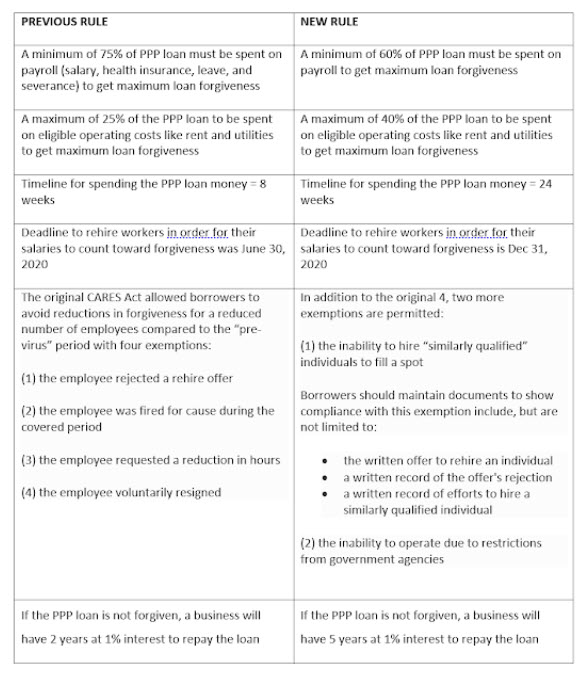

There are great financial rewards to obtaining full forgiveness of the PPP loans that sustained your practice during the lockdown. Here are the most recent updates to the rules you need to follow to increase the likelihood of loan forgiveness. Click HERE to download a PDF of the chart, allowing for an easier-to-read view.

Borrowers are able to submit an application for PPP loan forgiveness at any point after they have spent the entire amount of their loan. There is one caveat: If the borrower does not apply for PPP loan forgiveness within 10 months after the last day of the covered period, then the loan will no longer be deferred, and the borrower must begin making payments.

Borrowers should also realize that if any employee’s wages were reduced by more than 25 percent, they must account for this during the full eight- or 24-week covered period. As long as the borrower maintains the same employee headcount at the same pay rate as was in the original PPP loan application (or restored employee headcount levels or pay rates using the FTE Reduction Safe Harbor) through the PPP loan forgiveness application, there does not appear to be reduction in loan forgiveness. After that time, the borrower can then adjust either headcount or pay rate as best fits their business.

For clarification, the borrower has the option to choose the eight-week or 24-week period. It does not automatically convert to 24-weeks. Also, the changes in loan maturity of the PPP loans are not automatic. They are subject to lender and borrower approval. And you should be aware if PPP loan forgiveness is denied, the borrower has to start making payments on the loan.

Be on the lookout for further clarification and guidance. Questions that still need answers are:

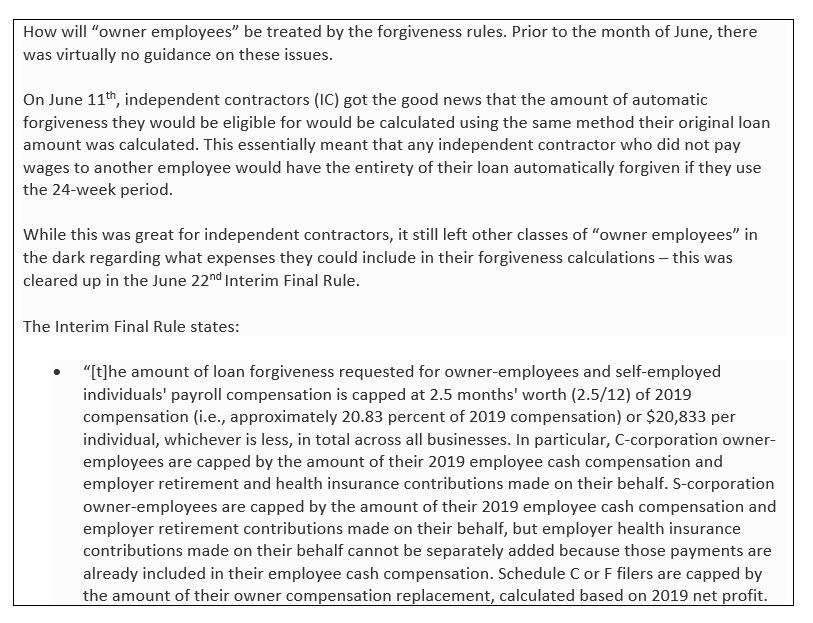

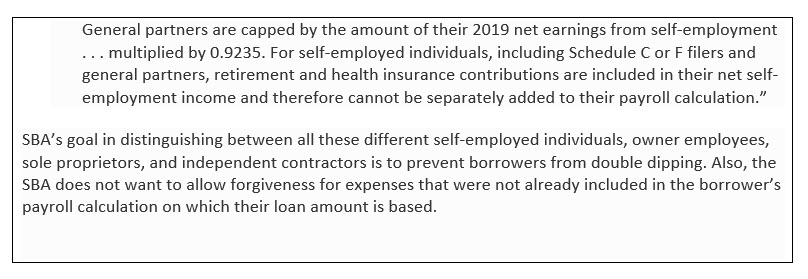

• Independent contractors cannot include their own retirement or health insurance contributions, but what is the difference between an independent contractor who files a schedule C and a C-corporation owner-employee?

Other Articles to Explore

• Forgiveness for owners (including S or C Corporation shareholders) will be limited to 15.385 percent for the eight-week period or 20.833 percent for the 24-week period of their 2019 compensation. There is no mention of limiting retirement plan contributions attributable to the shareholder employee of a company to 20.833 percent of 2019 contributions for such shareholder, which is provided for in the EZ forgiveness application. Is this limitation an error that will be deleted from the EZ application?

References

i. https://home.treasury.gov/system/files/136/PPP-IFR–Revisions-to-the-Third-and-Sixth-Interim-Final-Rules.pdf