What patients see when they enter Dr. Kling’s office. Dr. Kling says there are key differences between your profit-and-loss statement and your cash flow, which need to be taken into consideration as you manage your finances.

An important distinction to understand in your financial management.

By Mick Kling, OD

April 17, 2024

Years ago, I received a phone call from my CPA. He enthusiastically told me he had just wrapped up my taxes for the year and the practice was performing better than ever. We were growing, the schedule was full and we were consistently hitting our revenue goals.

Then, almost as an afterthought, he told me I would need to write a $25,000 check to cover the taxes for the year. I panicked…then did what most of us do and pulled out my mobile phone to check my bank balance. And as expected, my bank account was a long way from having the funds needed to cover the tax liability.

Out of desperation, I called my CPA a few days later to reluctantly admit I didn’t have the cash to cover the taxes. He said, “That’s easy, just go buy a commercial vehicle.” What? A commercial vehicle? I wasn’t really in the market for a truck. He went on to explain that all I needed to do was go to the local BMW dealership and tell them I was sent by my CPA to buy a commercial vehicle. And so I did, and walked off the lot with a brand new, shiny BMW X5.

As it turns out, the IRS tax code allows business owners, under certain circumstances, to purchase vehicles above a certain weight and deduct a portion of the purchase price to reduce taxes. While this turned out to be a great tax strategy, what I didn’t realize was the impact that another $1,000 monthly loan payment would have on my practice. While my tax situation improved, my cash flow worsened. I had successfully gotten myself out of a short-term tax problem, but created further long-term cash flow problems for myself by adding more debt.

In that experience, I learned a valuable lesson in the difference between “profit” (as reflected on a profit-and-loss statement) and cash flow. I learned that it’s possible to have “profit” (on paper) and no cash, in this case, to cover the taxes. And that profit is a measure to determine our tax burden while cash flow allows us to pay the ongoing expenses of the business.

Profit Defined

Profit is simply the difference between the amount earned (revenue) and the amount spent (expenses) in a business. It’s what’s left over after all the bills are paid. There are primarily three different types of profit reflected on a profit-and-loss (P&L) statement. These include: gross profit, operating profit (operating income) and net profit, sometimes called “the bottom line” since it’s usually the last number at the bottom of the P&L statement.

Gross Profit represents what’s left after cost of goods sold (COGS), your cost for frames, lenses/lab fees and contact lenses, are deducted from the revenue of the practice.

Operating Profit, sometimes called operating income, is the result after further taking into account the operating expenses of the business such as marketing, office supplies, bank charges and insurance, including the non-cash “expenses” of depreciation and amortization (See Sidebar).

Net Profit is what’s left over after all expenses are paid including interest on any debt and taxes.

What is Depreciation & Amortization?

Depreciation: The reduction in value of a tangible asset over time due to wear and tear of the asset. It is an accounting method used to allocate the cost of the asset over its useful life.

For example, let’s say you purchased a piece of new equipment for $50,000, which has a useful life of five years. This means that you could depreciate (deduct from your income) the equipment at a rate of $10,000 per year over the next five years, even though you may have paid $50,000 in cash or borrowed money for the equipment. In accounting, this is considered a “non-cash” expense since it does not actually involve a cash transaction. While this is a very simple example, it’s important to understand there are many nuances and exceptions when it comes to depreciating assets. This is where your CPA or accountant will come in handy.

Amortization: In accounting, amortization has two meanings. The first is spreading payments out over a period of time, such as for a home or car loan. The second meaning, similar to depreciation, is allocating the reduction in value of an intangible asset over time. Examples of intangible assets that may be amortized, and therefore, deducted from income include goodwill, patents, franchise agreements, copyrights and trademarks.—Mick Kling, OD

Cash Flow Defined

Cash flow is the soul of your business. It represents the inflow and outflow of cash, which allows you to pay your day-to-day operating expenses and stay in business.

Cash flow is all about timing, and cash flow management is collecting as fast as you can and paying as slowly as you can. A cash flow statement, like a P&L statement, is a financial report that shows the change in cash over time by recording the inflow and outflow of money.

The challenge with cash flow management is ensuring that more money flows into your business than out of it during any given period of time. For OD business owners, this can be a real challenge since we often deliver care first, then rely on third-party payors in hopes of getting paid at some future date.

Understanding the Difference

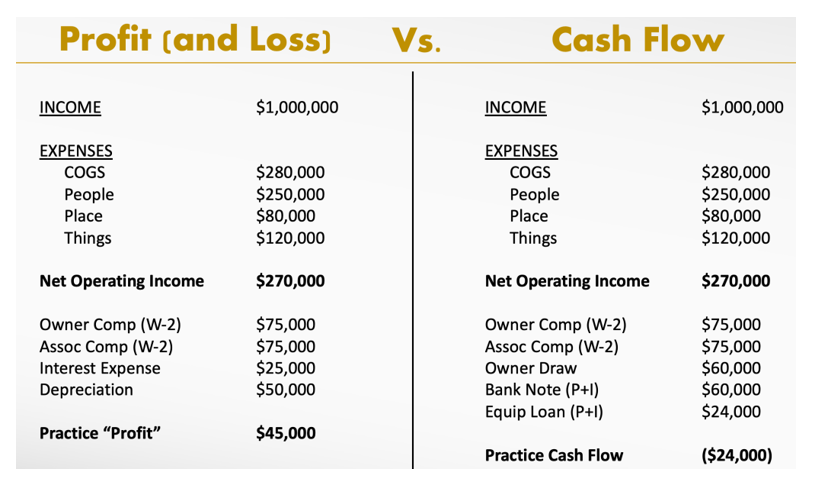

It might be best to show the difference between profit (as reflected on a P&L statement) and cash flow of a business by reviewing the example below.

On the left side, you will see a typical P&L statement. In this example, the practice generated $1,000,000 in practice income. After subtracting COGS and operating expenses, the practice shows a net operating income of $270,000.

We then deduct expenses for doctor compensation, interest on debt and depreciation. The result is what we are calling “practice profit.” This is the net profit (before taxes) of the business. (NOTE: In this example, we are reporting the net operating income before doctor compensation, interest and depreciation to stay consistent with the common practice of measuring the “optometric net,” in this case, $270,000, or 27 percent of revenue).

Other Articles to Explore

Now let’s take a look at the cash flow (right side) of the chart. You will see the same practice revenue ($1,000,000), COGS and operating expenses reflected with the same net operating income of $270,000. We also see the same W-2 wage earned for both the owner and associate doctor. There are now three additional expenses reported: an owner draw of $60,000, a bank note for $60,000 and an equipment loan for $24,000 with a practice cash flow loss of $24,000.

And therein lies the most important concept to understand about the difference between profit and cash flow. A P&L statement does not record distributions taken out of the practice and the principal payments made on debt. Both distributions and principal payments on debt come from the profit of the business. Distributions taken by the owner and principal payments made on debt are true cash expenses. It’s cash leaving the bank account, reported as “Profit” on the P&L statement, and is subject to taxes. This is why we can have “profit” and no cash to pay the taxes.

It’s worth remembering our CPA’s job is to help file our tax returns and minimize our tax burden. They often make recommendations to reduce our profit, such as encouraging us to spend money, since the only way to lessen the impact of taxes is to minimize profit. While this strategy can be useful, it’s important to remember the impact on cash flow, especially if borrowing money, and that our objective as business owners (make more profit) is sometimes at odds with our CPA’s objective (make less profit) to reduce taxes.

The best strategy for preventing year-end tax surprises is to have a plan (Profit First!) and communicate with your CPA frequently. Be mindful of how debt is impacting your cash flow, and how using your business bank account as a personal ATM machine can create cash flow problems.

Now that you have a better understanding of the difference between profit and cash flow, you might be less tempted by your CPA’s recommendation to buy that “commercial vehicle,” even if it is a BMW.

M ick Kling, OD, is the president of Impact Leadership and the founder and CEO of Invision Optometry in San Diego, Calif. Dr. Kling is also the Practice Management and Transition Advisor for Vision Source. To contact him: dr.kling@invisioncare.com

ick Kling, OD, is the president of Impact Leadership and the founder and CEO of Invision Optometry in San Diego, Calif. Dr. Kling is also the Practice Management and Transition Advisor for Vision Source. To contact him: dr.kling@invisioncare.com