By Mark Wright, OD, FCOVD,

and Carole Burns, OD, FCOVD

August 5, 2020

The Small Business Administration (SBA) issued an update to its rules for applying for Paycheck Protection Program (PPP) loan forgiveness. Here is what you need to know.

The SBA published its “Procedures for Lender Submission of Paycheck Protection Program Loan Forgiveness Decisions to SBA and SBA Forgiveness Loan Reviews” to all SBA employees and Paycheck Protection Program Lenders on July 23, 2020.i

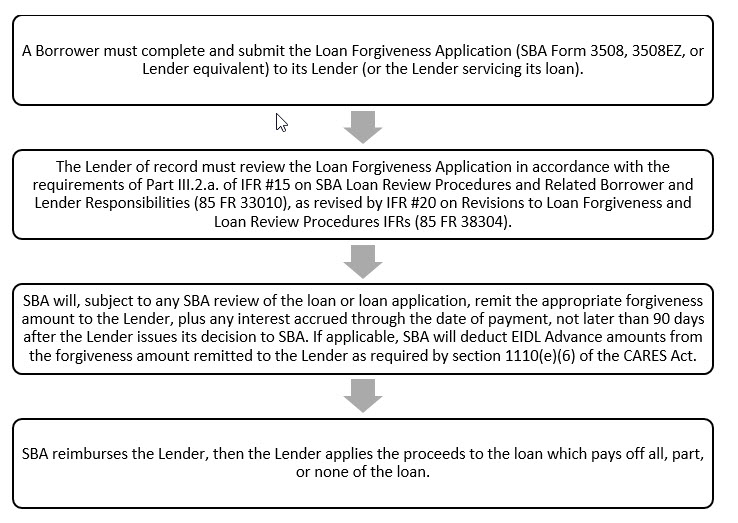

The goal of the PPP Loan Forgiveness process is to get maximum forgiveness for the Borrower. To make that happen, it is important to understand the process. This chart gives a summary of the four-step process.

Determine Your Eligibility for Forgiveness

The Borrower is responsible for determining their eligibility for using the SBA Form 3508EZ or SBA Form 3508 based on page 1 of the SBA Form 3508EZ instructions. (Lenders are unlikely to tell the Borrower which application to use as this is a Borrower directed loan program based on certifications by the Borrower.)

There should be limited back and forth between the Borrower and the Lender as the PPP Loan Forgiveness Applications disclose in the instructions the documentation that must be submitted with the application and the documentation the Borrower needs to retain for their records. Lenders should not have different requirements for documentation as SBA sets the documentation requirements as addressed in the PPP Loan Forgiveness Application instructions. Borrowers should look to page 4 of the SBA Form 3508EZ instructions and page 6 of the SBA Form 3508 for documentation guidance.

Borrowers should also look to the U.S Department of Treasury web site for additional guidance before contacting their Lender with questions. This site is the most organized and comprehensive source of information versus the SBA’s web site.ii

Other Articles to Explore

This is a Borrower-directed loan program that is reliant on Borrower certifications, applications and documentation with the liability for such based solely on the Borrower. Lenders are relying on the information provided by the Borrowers and are unlikely to provide guidance outside of what is disclosed in the regulations.

The Lender has 60-days after receipt of a complete Loan Forgiveness Application to review the loan application before issuing a decision on forgiveness to the SBA.

Loan Forgiveness Submission

According to the SBA document, “a Borrower may submit a Loan Forgiveness Application before the end of the eight-week or 24-week covered period, provided that the Borrower has used all of the loan proceeds for which the Borrower is requesting forgiveness and the Borrower’s Loan Forgiveness Application accounts for any salary reductions in excess of 25 percent for the full covered period.”

You should know that the SBA is not accepting Loan Forgiveness Applications from Lenders until August 10, 2020. This has the practical meaning that no loan applications have been processed by the SBA to date even though Loan Forgiveness Applications have been submitted to Lenders by Borrowers. SBA indicated that this process is subject to change by any new legislation. This information does not mean that you should wait to submit your Loan Forgiveness Application to the Lender.

Follow the rules and make sure your documentation is exactly what is required.

References

i. SBA Procedural Notice, CONTROL NO.: 5000-20038, EFFECTIVE: July 23, 2020

ii. https://home.treasury.gov/policy-issues/cares/assistance-for-small-businesses