Adam Cmejla, CFP® with his family in a plane he is piloting. There are parallels, he says, between the principles behind long-term financial management and some of the principles of aviation.

By Adam Cmejla, CFP®

Jan. 12, 2022

One of my life’s passions is aviation. There’s something magical about what we’ve been able to do as a species to create amazing machines that are able to transport us through the skies at all speeds and altitudes. It’s captivated me since childhood. As a financial planner who specializes in working with optometric practice owners I have noticed parallels between what is needed to safely land a plane and what is needed to safely land a private practice into a financially secure future and eventual sale.

What Goes Up Must Eventually Come Down

Ask any (good) pilot what the secret to a perfect landing is and they will most likely answer something like this: “A perfect landing starts with flying a perfect pattern.”

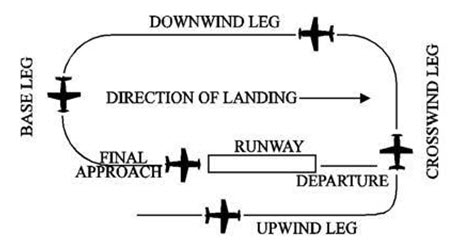

For an airplane that is coming in for landing at an airport, the three legs of the descent, shown on the image below, are the downwind, base and final approach. Even before a pilot enters the pattern, they’re always running through a variety of checklists to ensure that they haven’t missed anything that’s required to make a safe and consistent landing.

Notice the key words in the last sentence: safe and consistent. Is it possible to land an airplane without following the proper procedures and checklists? Sure. Is that an airplane I would like to be a passenger on? Nope.

Small Decisions that Add Up to Big Final Result

What does flying a safe and consistent perfect pattern to have to do with financial planning for ODs? It’s a great metaphor to emphasize how a series of small, seemingly insignificant tasks done correctly compound to produce a successful result…and how missing those tasks or not anticipating them can lead to unanticipated results at best or accidents and disasters at worst. Let’s go through the different phases of landing an airplane and correlate that to financial planning actions.

Entering the Pattern on the downwind leg. Proper communication is key when flying. When flying at a non-control towered airport, radio calls are made to announce who you’re talking to, who you are, where you are and what you want to do. This lets other pilots in the area start to visualize where you are in the airspace so they can plan their moves accordingly. Even before the pilot is in the pattern, they’re taking inventory of not only other traffic in the area (variables outside of their control) but also gauges inside the cockpit such as fuel, engine performance, airspeed and altitude (variables under their control).

Just as communication is important in flying, so too is it in financial planning. Proper communication serves many benefits to multiple parties. It’s important to communicate your goals and intentions with not only your family (spouse, kids, etc.), but also with the other key advisors and relationships in your life. You should be able to accurately state not only where you are currently, but also where you want to go and what you want to do. You can’t just “think” or “wish” your way to financial independence. Everyone wants financial independence, but there’s a difference between wanting it and being willing to do the tasks and planning necessary to get there. Harvey Mackay says that “A dream is just a dream. A goal is a dream with a plan and a deadline.”

Turning base and final approach. Turning onto your base leg is a key position in the landing process. You want to make sure two measures are on target: airspeed and altitude. The interesting thing about the base leg, though, is that the consequences of NOT hitting your numbers really aren’t felt at this point in the landing process. If you “didn’t know what you didn’t know” you’d think that everything was still going just fine…you’re on your way to the airport.

Here’s what’s interesting, though. The compounding effect of missing those numbers on your base leg really shows up when you turn onto final approach. Too high and fast and now you have the task of trying to dissipate altitude by reducing power while maintaining a stabilized approach and attitude. Too low and slow and you’ll be adding power to maintain altitude while maintaining attitude. While there’s already enough to be cognizant of while landing, you now have an additional workload to manage.

All of this is happening as the runway gets closer and bigger in your windscreen. The margin of error gets smaller, your ability to correct these miscalculations reduces and the evidence of your errors is amplified.

Other Articles to Explore

In the end, though, the pilot always has one last arrow in the quiver: the go-around. If she doesn’t like the way things are setting up, she’ll add full power and initiate a climb to go around and give it another try.

Your Financial Destination is Getting Closer & Closer

However, in financial planning, you don’t have the option of a “go around.” The runway (retirement, financial independence…call it what you will) is getting closer and closer with each passing day, week, month and year. The closest thing OD practice owners have to an arrow in the quiver is the equity value they have in their private practice. The traditional private practice with a standalone location, which may also own the real estate and building, will have a certain amount of value, but in my experience working with ODs, (a) it’s usually a lot less (after taxes) than the OD thought it would net them and (b) it can be even lower if the practice isn’t run efficiently and “primed” for a sale.

So, while both the pilot and standalone private practice may have their respective versions of a “go around” always available, the pilot is the only one truly with the option of an actual “do over” to obtain the same originally desired result or a safe landing.

The two key variables in the landing pattern are altitude and airspeed. Hit those numbers at the key points and the chances of having a smooth and uneventful landing are significantly increased.

In retirement planning, we can replace airspeed and altitude with “time and savings rate.” Savings rate is the amount of your gross income you are saving for retirement. Time is the number of years between when you first started saving for retirement and your goal of being financially independent.

Make sure you understand the impact of these two most important variables in your financial plan, so you don’t need to “go around” when going around isn’t an option.

Adam Cmejla, CFP® is a CERTIFIED FINANCIAL PLANNERTM Practitioner and Founder of Integrated Planning & Wealth Management, LLC, an independent financial planning & investment management firm focused on working with optometrists to help them reach their full potential and achieve clarity and confidence in all aspects of life. For a number of free resources, visit https://integratedpwm.com/ebooks/ and check out the “20/20 Money Podcast” to get more tips on making educated and informed financial and business decisions.

Adam Cmejla, CFP® is a CERTIFIED FINANCIAL PLANNERTM Practitioner and Founder of Integrated Planning & Wealth Management, LLC, an independent financial planning & investment management firm focused on working with optometrists to help them reach their full potential and achieve clarity and confidence in all aspects of life. For a number of free resources, visit https://integratedpwm.com/ebooks/ and check out the “20/20 Money Podcast” to get more tips on making educated and informed financial and business decisions.