Photo credit: Getty Images

Third and final article in a three-part series on managing student debt.

By Evon Mendrin, CFP,® CSLP®

May 8, 2024

With increasing levels of student loan debt, a critical planning point for every optometrist is deciding the best approach to tackling the debt.

Fortunately, there are a few key approaches, depending on your goals and circumstances. The first article in this series addressed the approach of paying the loans off entirely. The second article reviewed the advantages of student loan forgiveness with income-driven repayment plans.

This third and final piece in the series will explore the advantage of taking a hybrid approach to managing student debt, and will wrap up the series with overall points to consider when it comes to student debt.

Highly Focused Use of Income-Driven Repayment Plans

There may be specific situations – particularly in the early years of your career – where you want to prioritize having more flexibility in your cash flow each month.

Some examples of where you’d want that extra wiggle room:

- Buying a home

- Cold-starting or purchasing a private practice

- Prioritizing building your emergency fund or another short-term goal

- Sudden changes in your income vs. expenses

In such cases, it may make sense to put dollars toward other priorities rather than pay aggressively into the debt. For example, building savings for emergency funds, house down payments, or other important shorter-term priorities are part of building a sound financial foundation.

When seeking a home or practice loan, lenders consider your available cash flow and debt-to-income ratio during the underwriting process. Moreover, having additional cash flow flexibility and a bigger savings account can alleviate financial stress in the early years of practice ownership.

In these cases, you can strategically use an income-driven repayment (IDR) plan to temporarily lower your student loan payments, use the extra dollars as needed, then flip the switch down the road to more aggressively tackle your student loans.

Other Articles to Explore

Since those payments are based largely on your income and family size, they’re especially helpful during times when income is unusually low – such as right after graduation or when cold-starting a practice.

The SAVE IDR plan is an ideal option in this scenario. It will likely have the most favorable payment calculation, and there is no accruing unpaid interest. You’re essentially “freezing” your student loan balance.

Once cash flow is stable, you can choose the best long-term approach to planning around the debt.

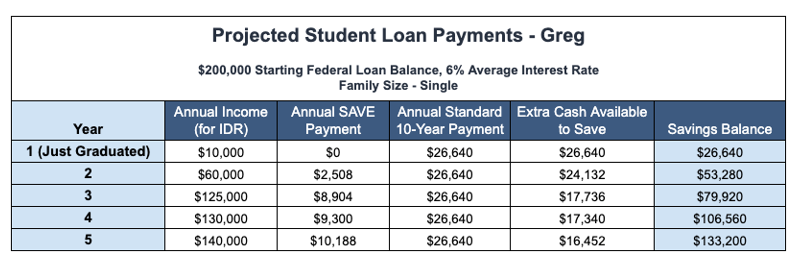

For example, let’s say Greg just graduated from optometry school with $200,000 of federal debt. In his fourth year of optometry school, he filed a tax return with a small amount of part-time work. In his first year of practice, he only worked a half-year, so his income was very low. Greg’s planning to work at a private practice for five years before buying into the practice. He may plan to purchase a home as well, but it’s not the top priority.

How would the math play out if Greg used the SAVE plan right out of school, using the tax return filed during college to calculate the first year’s payments?

Due to very low income the first two years, Greg enjoyed low loan payments under the SAVE plan. By year five, he was able to use the extra cash to save over $100,000 in a high-yield savings account.

He’ll have a lower debt-to-income ratio for loan approval, and the extra savings puts him in a much better position financially for the early years of practice ownership. And when he’s ready, he can flip the switch and pay down the same $200,000 loan balance more aggressively.

What if he decides not to go into ownership? He can use the savings balance to make a lump-sum payment into his loans and end up in roughly the same position had he started payments from the beginning (since SAVE doesn’t accrue the unpaid interest). Or, he can use the cash for other goals – like that house down payment – or for investing.

The bottom line is he was able to create additional flexibility month to month by lowering his required minimum loan payments, build his cash savings, then decide on next steps from there.

Conclusion – How to Decide the Right Approach For You

The right approach for you depends on many factors unique to your situation:

- Amount and types of federal loans vs. income – debt levels vs. income (or expected income) is a big part of the forgiveness vs. pay-down math. Total debt above 1.5x your income is when I start reviewing forgiveness seriously.

- Family size, marriage and future children – a higher family size can lower IDR payments.

- Spouse’s income and federal student debt – spouse’s income can increase IDR payments, and a spouse’s federal loans impact how IDR payments are calculated.

- State of residence and how you file taxes – married borrowers who file taxes separately may improve the outcome toward forgiveness. But it also adds tax considerations. There are potentially more planning opportunities in community property states (e.g., CA, TX, WA, etc.) for spouses filing separately, since income is split for tax purposes.

- Your unique cash flow needs and career goals – what are the top life and money priorities right now? Do you need a place to live? Is practice ownership on the horizon? Do you have the foundational planning actions handled before paying aggressively?

- Your feelings, values and preferences around debt

Like many financial decisions, it comes down to a mix of what the math says is likely to be optimal with how the future might unfold, versus your values and feelings about debt.

Some prefer to use cash flow now and are willing to stick with the 20-year plan. Others want to pay it aggressively, regardless of what the math says.

Student loans can be complicated, and they may seem like a barrier to reaching your financial and career goals. But with the right guidance, action and mindset, there are plenty of opportunities to put yourself in the best position financially.

Evon Mendrin, CFP®, CSLP® is the founder of Optometry Wealth Advisors, an independent financial planning firm serving optometrists nationwide. You can contact him at evon@optometrywealth.com, and check out The Optometry Money Podcast, helping ODs make better decisions around their money, careers and practices.

Evon Mendrin, CFP®, CSLP® is the founder of Optometry Wealth Advisors, an independent financial planning firm serving optometrists nationwide. You can contact him at evon@optometrywealth.com, and check out The Optometry Money Podcast, helping ODs make better decisions around their money, careers and practices.