Photo credit: Getty Images

The second of a three-part series on how best to pay off your student loans. Click HERE to read part one.

Evon Mendrin, CFP,® CSLP®

March 13, 2024

With the rising costs of education, choosing the right approach to tackle your student loans has never been more important. Ideally, you’re balancing three factors: minimizing your total costs, your current cash flow needs and your values about debt.

Fortunately, there are a few key approaches to tackling debt. The first article in this series addressed the approach of paying the loans off entirely. This article will give a basic overview using income-driven repayment (IDR) plans toward federal loan forgiveness.

Mathematically, this approach can make sense if you have high federal student loan balances relative to your income (or expected income) or plan to work for a nonprofit.

It’s fundamentally different than traditional debt management – you are intentionally trying to pay off as little debt as possible so that as much of it is forgiven as possible. You have no intention to pay the debt down.

And there are certainly planning opportunities to lower your income for student loan purposes and improve the outcomes.

How IDR Plans Work

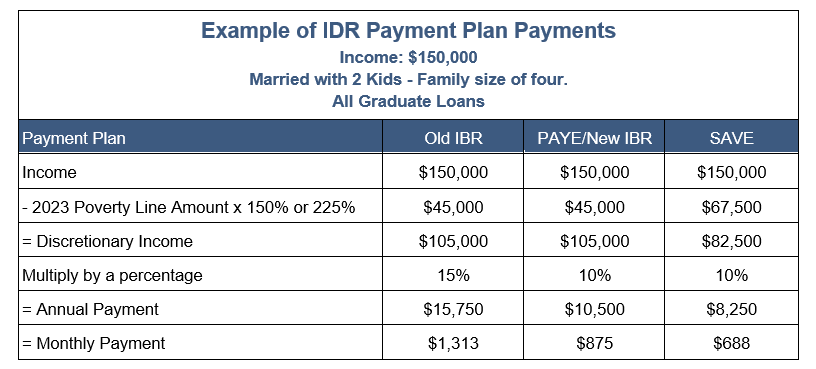

Unlike most debt payments, IDR plans calculate your payments based only on your income and family size – the debt size and interest rate don’t matter.

The calculation starts with your income (by default the AGI on your most recent tax return), subtracts out a poverty line amount for your family size, then multiplies that result by a percentage to get your annual payment. Each year, you provide your updated income and family size to recalculate your payments.

There are five different IDR plans, each with their own details, calculations and rules for eligibility. After making payments for a certain number of years, the remaining debt balance is forgiven.

The plans optometrists will likely be concerned about moving forward are:

- Pay As You Earn (PAYE) – 20 years until forgiveness.

- New Income Based Repayment (IBR) – 20 years until forgiveness

- Saving For a Valuable Education (SAVE) – 25 years until forgiveness

Eligibility is based on the type of debt you have and when you first received federal loans.

As payments are based on your income and family size, a key part of this approach is working to lower your taxable gross income over the years. This can be done by using most methods of tax planning to lower your AGI. For example:

- Pre-tax retirement accounts like 401(k)s and SIMPLE IRAs

- Health Savings Accounts

- Deductible business expenses and depreciation

- Various potential real estate tax planning

- Other pre-tax deductions, like health insurance premiums for employed ODs or spouses.

There are two main types of loan forgiveness:

Public Service Loan Forgiveness (PSLF)

PSLF is available for optometrists working with government employers and non-profits. After 120 “qualified” payments (10 years) on direct federal loans, using IDR plans, while working “full time” for these employers, the debt is forgiven tax-free.

Due to recent rule changes, PSLF is also available to optometrists who cannot work directly for the nonprofit due to state laws – such as Kaiser Permanente in California.

Taxable Forgiveness

Practice owners and ODs with private employers can benefit from taxable loan forgiveness.

You receive forgiveness after 20- or 25-years of IDR payments. Under current tax law, forgiven federal loans after 2025 will be taxable income in the year of forgiveness. To prepare for that future tax, you can invest each month into a taxable brokerage account.

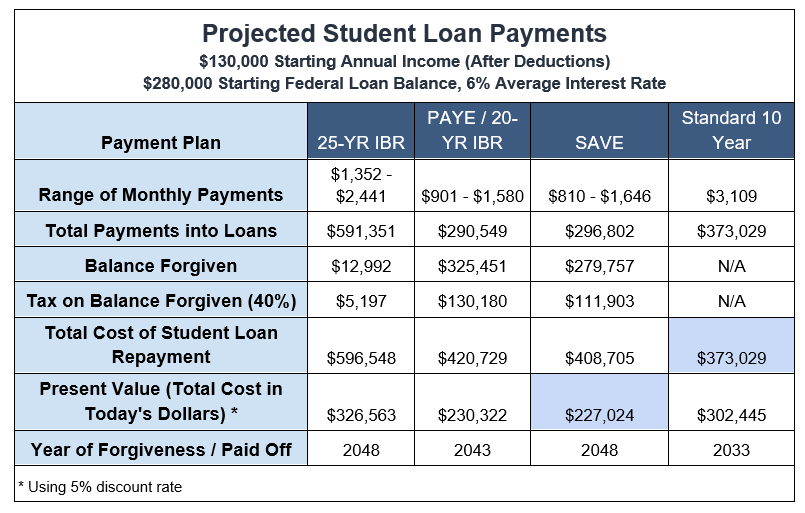

Consider the example of a recent grad. This OD starts with an annual income (after pre-tax deductions) of $130,000, and it’s expected to increase 3 percent per year. He has a federal student loan debt of $280,000, and is eligible for all IDR plans. Assuming he stays single, how does the math work out?

What’s the Best Loan Option to Take?

The standard 10-year repayment plan has the least projected total cost. However, the best course of action from the math is likely the SAVE plan for 25-year forgiveness.

Why? SAVE has a lower cost in present value – meaning the total of all the years of payments plus the projected tax, brought into today’s dollars.

Other Articles to Explore

Comparing the present value of the total cost is a more effective way to compare different repayment plans over very different time periods (10, 20, 25 years). It reflects the fact that there’s a time value to your money.

Future dollars are worth less than dollars today, due to the natural effect of inflation as well as your ability to use and invest your cash right now to earn a return.

Even successful practice owners can benefit from loan forgiveness with the right planning. There are many factors that can change and improve the math for IDR plans:

- Change in income and use of pre-tax deductions

- Change in family size – marriage and children

- Whether your spouse works and/or has federal student loans

- How you file taxes (married jointly or separately)

- Whether you’re in a community property state or not

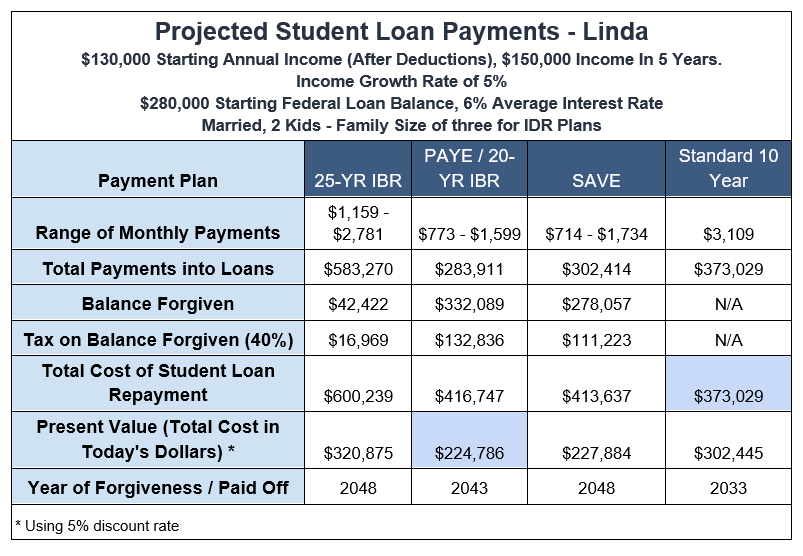

For example, take George and Linda, married with two children. Linda is planning to purchase a successful practice, and her income is expected to go from $130,000 (after deductions) to $300,000 in five years. George plans to stop working and stay home with the kids for an extended period. Linda has $280,000 of federal loans, and George has none.

On the surface it appears Linda should pay down her debts aggressively. With an income expected to be above her starting loan balance, you might assume she won’t benefit from forgiveness.

However, George and Linda live in a community property state (Calif., Ariz, Nev. and others). This allows them to file taxes separately, and their AGI will be split evenly on their tax return – making Linda’s income for student loans $150,000. This doesn’t include any tax planning she’d consider to lower her income even more. So, the results may look like:

The ability to file taxes separately and split community property income is a huge planning opportunity, allowing Linda to take advantage of IDR plans and additional cash flow flexibility.

Even in non-community property states, it may make sense to file separately to exclude your spouse’s income from the calculation. Of course, there are also tax impacts of filing separately to project and consider.

What if George also had federal loans? He can self-certify that he doesn’t have income, bringing his payments to $0.

What if George worked? He can use his pay stubs as income documentation. This creates more opportunities to shift any available pre-tax deductions to his pay stub and lower his payments.

The couple would show their income each year, identify which form of income to use and whether to extend tax filing, work to lower their taxable income and payments with deductions, and prepare for the future tax.

There are more opportunities than meet the eye. The details and nuances of each repayment option, what factors impact the results, and how to interpret and act on the results are all important to making the right decisions. It’s all specific to your situation.

Lastly, keep in mind two important upcoming IDR deadlines in 2024:

- The one-time IDR account adjustment deadline to consolidate your loans by April 30, 2024, and

- Losing access to PAYE after July 1, 2024, unless already on it.

Evon Mendrin, CFP®, CSLP® is the founder of Optometry Wealth Advisors, an independent financial planning firm serving optometrists nationwide. You can contact him at evon@optometrywealth.com, and check out The Optometry Money Podcast, helping ODs make better decisions around their money, careers and practices.

Evon Mendrin, CFP®, CSLP® is the founder of Optometry Wealth Advisors, an independent financial planning firm serving optometrists nationwide. You can contact him at evon@optometrywealth.com, and check out The Optometry Money Podcast, helping ODs make better decisions around their money, careers and practices.