By Adam Cmejla, CFP®

Sept. 19, 2018

In my last article, “Keys to Financing a New Practice,” I reviewed tips for creating a business plan for your new practice, and a few points to think about when attempting to secure loans.

Now, let’s dive deeper into financing situations, and options, that each OD could consider, and let’s evaluate those options throughout the hypothetical life cycle of a practice.

Specifically, let’s make the following assumptions as our OD graduates through different stages of her professional career:

• Early on and shortly after graduation, she starts up her practice cold

• Ten years later, an opportunity presents itself to buy a practice from a close-by retiring doctor.

Through this example we’ll be able to see the end result of business decisions that are made in the beginning of her career, and use that information as lessons we can learn from in our own lives.

The Startup (Age: 30)

After practicing in a commercial setting for about three years, our recent graduate opts for entrepreneurship and decides to start a practice cold. For those of you who want to start a practice, it’s important to understand that there are lenders out there that can lend up to 100 percent financing for the startup of a practice. The proceeds of the loan can be used for normal startup costs such as equipment, leasehold improvements, software and working capital.

An important distinction in the definition of your practice: 100 percent financing is not available for the purchase of any real estate. For those purchases, you will be required to bring money to closing. However, some lenders can get creative with financing options. The important distinction is that your practice note will only be for what’s “inside the walls” of your practice. The purchase of the building is a separate purchasing and financing transaction.

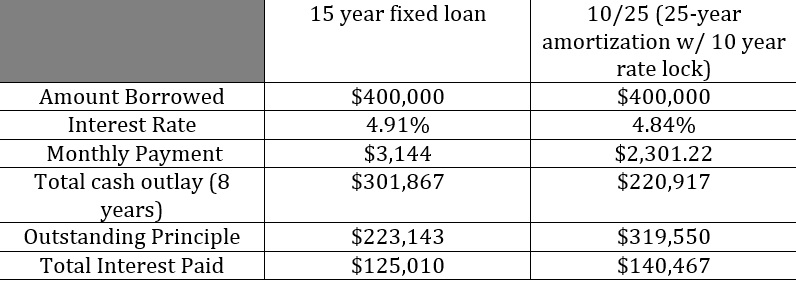

There are many different factors to consider when estimating the cost of starting a practice cold in a leased space (no real estate purchase), but let’s make a general assumption that she was able to open the doors with $400,000 and assume that she does not have any capital to bring to the table. She practices for eight years before being presented with a great opportunity.

Here’s a look at two options for financing that purchase:

The Acquisition & Consolidation

Our OD is presented with an opportunity to buy another local OD’s practice, as he has decided to retire from optometry altogether. Unfortunately, the selling doctor did not do a good job of preparing his practice for transition: his revenues have been declining the last four years, he hasn’t modernized the practice (very little new technology), and has an unhealthy income statement showing higher-than-normal overhead expenses.

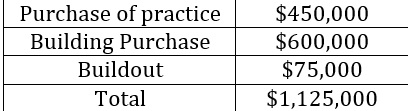

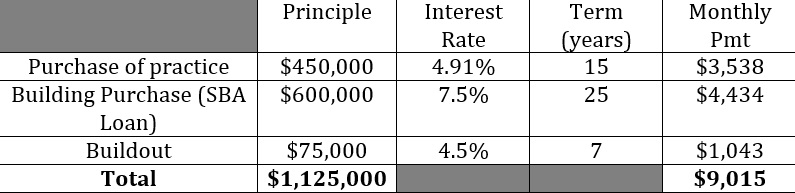

Because of this, let’s assume that our OD has the ability to purchase his practice for $450,000 as an asset purchase.

Given the size of the practice, our OD decides that neither practice is big enough to be housed in two separate locations, and they are close enough geographically that merging them together into one new space is the best decision.

Coincidentally, she finds an old daycare center a half mile from her location that is available for sale. She has the opportunity to purchase the building for $600,000, and it requires $75,000 in build-out costs.

Summary of transaction:

Because the building is a commercial real estate purchase, she will need to bring at least 10 percent as a down payment. Let’s assume that she’s been able to accumulate $60,000 in personal savings, and is able to make the down payment.

She is now at a decision point because she can’t forget about the outstanding debt that she incurred starting her own practice.

Depending on which route she went in the beginning, she’s still going to have either $223,143 or $319,550 remaining on her balance sheet…and if it’s the latter number, she’s going to have a balloon payment due in two years or she’ll have to refinance at current interest rates if she wants to continue that amortization schedule. All will have to be considered to see if this opportunity is affordable.

A general rule of thumb is to keep your monthly debt service payments at, or below, 1 percent of outstanding debt. In addition, loan originators will look at something called the “debt service coverage ratio” (DSCR) to determine how healthy your practice is from a cash-flow perspective. This ratio is your net operating income (NOI) divided by your annual debt payment. The higher your DSCR, the better and healthier your business looks to an underwriter.

Given this information, her monthly debt service payment is going to be either $12,159 or $11,316 depending on whether she elected to finance her original startup on either a 15-year fixed or 10/25 note structure, respectively. The rate is fixed for the first 10 years of the note, but the loan is amortized over 25 years. That means, in the tenth year, the loan will either require a balloon payment (paid off in full) or a refinancing of the loan based on current interest rates.

For this deal to go through as is, our borrower would have to have net operating income of at least $215,000. If we assume that she can run her practice within the normal operating margins of today’s private practice, and is at a 28 percent profit margin, then she would have to ensure that the practice is producing at least $781,650 per year in gross revenue (collected). Given these metrics, we could ascertain that she is in a position to make this deal work, assuming that she is approved through underwriting. Moreover, we can also conclude that she has the opportunity to turn this into a very profitable practice.

Looking at another metric, her total monthly payment is less than 1 percent of her outstanding commercial liabilities. This is true regardless of the loan structure she took when she started her practice.

Keep in mind that all of this does not happen in a vacuum apart from the other circumstances of a well-executed financial plan. None of the above matters if our OD is not able to save 20 percent of her income in retirement plans and personal savings.

Cannibalizing the asset side of your personal net worth statement to make debt payments is no path to financial prosperity. They must both be done in tandem and unison, not at the expense of one another.

Business debt can be perilous, but it also can be a tool to facilitate business growth. The key takeaway from the examples outlined in this article: Understand the kind of debt that is useful to you, and the related decisions that can make it more manageable.

Adam Cmejla, CFP® is a CERTIFIED FINANCIAL PLANNERTM Practitioner and Founder of Integrated Planning & Wealth Management, LLC, an independent financial planning & investment management firm focused on working with optometrists to help them reach their full potential and achieve clarity and confidence in all aspects of life—personally, professionally and financially. For a free copy of his “Top Five Tips to Financial Freedom” visit https://bit.ly/2Mo3NV8.

Adam Cmejla, CFP® is a CERTIFIED FINANCIAL PLANNERTM Practitioner and Founder of Integrated Planning & Wealth Management, LLC, an independent financial planning & investment management firm focused on working with optometrists to help them reach their full potential and achieve clarity and confidence in all aspects of life—personally, professionally and financially. For a free copy of his “Top Five Tips to Financial Freedom” visit https://bit.ly/2Mo3NV8.