By Bob Schultz, President & CEO, Vision One Credit Union

SYNOPSIS

Most doctors are surprised at the initial low return of a second practice acquisition. Look at the entire picture, not just the initial return. Here are six tough questions to ask yourself to determine: Do I buy? Or walk away?

ACTION POINTS

SET GOAL. Ask yourself how much you want to make in exchange for the effort and risk of acquiring a second practice. Then quantify your goals.

SELECT A SPECIALIZED LENDER. Select and work with a lender who understands the unique dynamics of an optometric practice. Most lenders don’t.

BUY OR WALK The acquisition must meet your goals. Your time is finite and numbers don’t lie. If you can’t handle the deal, or the numbers don’t work, walk away.

Tough Question 1

“What do I want to get out of this acquisition?”

Have a candid conversation with yourself and ask bluntly: “What do I want to get out of this acquisition? How much money and potential value given the effort and risk will make it worthwhile?”

Are you willing to shoulder more work and take on debt just to make $10,000 or $20,000 more per year? Or is your goal $50,000 or $100,000 more in your pocket?

How does this fit in with your career goals and your retirement plan? Then locate the “tipping point” that makes the deal doable, according to your goal.

Tough Question 2

“What is my plan?”

What is your working plan if you acquire a second practice? Here are common scenarios for an acquired practice:

Maintain it. You can purchase outright, manage it independently, keeping on the present OD and staff as employees. Or hire a new OD to run it. Let present practice net cash flow pay for debt service and provide some profits.

Grow it. If a second practice has revenue streams that can be added or expanded, make a plan for that. For example, an older practice may be doinglittle medical model optometry. You may also bring more specialty services and be able to expand the patient base.

Roll it up. You can purchase a nearby practice and transfer patients to your practice, allowing you to eliminate competition, save on occupancy expense and run a single, larger practice.

Tough Question 3

“Reality check: Can I handle it?”

Small Practice. A very small practice may be too small everto be profitable. It may be a “roll-up” deal if the price is right.

Mid-Size Practice. If the practice you are considering buying is about the size of your present practice, it may be in your management comfort zone. Be aware that your attention will be bifurcated between the two practices.

Large Practice. Running large practices may exceed your management capabilities. Run the numbers: When does hiring an office manager or consultant make sense? Does it fit this deal?

Regardless of the size practice you might purchase, make sure your management and accounting systems are reliable and effective. It is more complex to run two practices as you cannot be at both locations all of the time. You will have a higher reliance on your system reports and key personnel.

It is best to maintain separate accounting for each practice. Also it will provide reliable accounting data if you choose to sell one of the practices.

Tough Question 4

“Does the deal work in terms of net cash flow?”

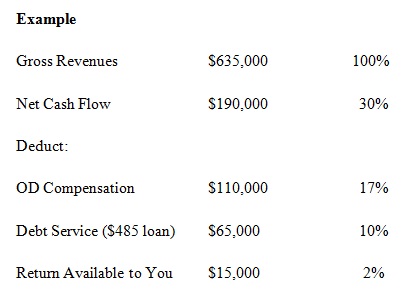

The key to understanding the profitability is practice net cash flow. This is also a primary metric used for practice valuation. Practice net cash flow is the collected gross revenue minus cost of goods sold minus overhead expenses. It should be viewed two ways:

1. Before OD compensation – identifies practice efficiency and allows comparison to MBA industry metrics.

2. After OD compensation is deducted – OD expense is real so it must be included to determine your return.

In our example, the presumption is that you are already working full time in your existing practice and must hire an OD for five days per week, regardless of which practice they work in.

To calculate practice return available to you, debt service, if the new practice is financed, must also be deducted as an additional step to the calculation above. The results can be expressed in dollars and percentage of collected gross revenues.

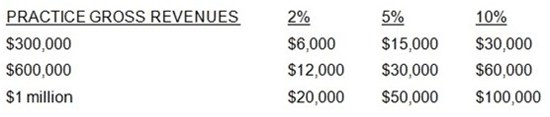

Is it worth the risk/effort to make 2 percent of gross? Or 5-10 percent of gross, if you can achieve that over time? The answer to this question may depend on the size of the practice gross revenue. Consider buying a larger or more efficient practice (higher net cash flow to revenue).

Also, time factors into this equation–in two ways.

First, duration before retirement: Multiply annual profits times 10-15-20 years before your retirement.

Second, time until debt is paid off: If you pay off the loan in 7-10 years at that point you add 10 percent, or $65,000 in our example, to the amount of money you can take out of the practice that had been going to debt service. A 2 percent net becomes 12 percent net. The return to you becomes $80,000 ($15,000 plus $65,000). That produces a far different picture. Also you should be creating additional cash flow over time as you build equity toward a practice sale upon retirement.

Tough Question 5

“What can I change that will increase revenues and net?”

Common scenarios that will increase revenues and net:

Add medical model. An older practice may be doing little or no medical. Can you add Medicare? Can you get on the local medical panels? If so, what is your estimate of the potential increase to gross revenues? Now re-compute net cash flow.

Consolidate office procedures. Consolidating billing and coding in one office and utilizing a common EHR/practice management system can yield cost savings and staff/time savings, once the transition is completed.

Lower Cost of Goods. If you can vault from being a $600,000 practice to one grossing over $1 million, you should be able to claim greater volume savings on optical goods. If the acquired practice is not in an alliance, joining one can lower COGS.

Add and Update Instrumentation / Higher Utilization of Existing Equipment. Having some of the latest diagnostic equipment should provide for a better exam and new billings. It may also position you to participate in AffordableCare Organizationsand other aspects of health care reform. But major purchases, when financed, require debt service. A quick and easy return on investment (ROI) analysis is needed to compare expected incremental revenue for the new procedures v. debt service. Determine projected incremental revenues from both practices if you do not currently own the instrument. Don’t “over buy,” as it will cost you. In many cases, the instrument may be shared by both practices.

Roll it up. You can purchase the practice for its patients and assets–then close it and combine patients and assets into your main location. You can save on some staff costs, rent and other expenses. In many situations it is best to operate in both locations for a year or so until the patients are committed to you, and then merge locations.

Adjust the sale price, debt service. If the numbers do not work but are close, you may be able to negotiate a lower sales price with a motivated seller. Alternately, you could put more cash into the down payment and lower your debt service to bridge the cash flow gap.

Tough Question 6

“Should I buy” Or walk away?”

In this final step, have the most candid conversation of all: “Do the numbers work? Does the cash flow from this deal meet my goals? Can I build significant wealth by paying off my second practice acquisition debt over time while ramping up the net cash flow and value of the new practice?

Can I reasonably manage two practices?

Or should I walk away?”

The tipping point is revealed ifyou can answer these tough questions.

Related ROB Articles

Getting There: Planning a Successful Optometric Career

Grow or Die: Complacency is a Practice-Killer

Bob Schultz is president and CEO of Vision One Credit Union in Sacramento, Calif. To reach him: BSchultz@visionone.org.