By Adam Cmejla, CFP(R)

Nov. 15, 2017

Savings for your retirement should begin on day one of your career. With careful planning, each phase of your career offers an opportunity to maximize savings–if you don’t let what I call “lifestyle creep,” or living beyond your means, get in the way.

If you’re not disciplined, lifestyle creep can cramp your ability to build adequate savings. It is the slow, but incremental, increase in your personal cost of living that can be the byproduct of having a successful practice, and not being mindful of personal spending habits. The“I’ll start later” excuse doesn’t cut it in saving for retirement. Life never gets less complicated or cheaper. Saving is a habit. Start now, and it’s a good habit that’s hard to break.

Let’s play out a hypothetical OD’s professional career trajectory, and see where mistakes in personal savings can occur, so you know what to be aware of in every stage of your career to ensure maximum savings.

The first 10 years (ages 26 – 36)

CALCULATE & MANAGE DEBT

The new OD has a substantial paycheck for the first time in their life and two well-earned letters after their name. Unfortunately, for most students, these initials also required them to take out significant student loans. Most of my young clients are saddled with anywhere from $150,000 – $275,000 in total student loan debt. (Fun trivia fact: our client with the biggest student loan balance? A dual physician couple that are tipping the student loan scales at $810,000).

PAY OFF DEBT FIRST, THEN AMERICAN DREAM

The new optometrist is also now feeling the urge to “live the American dream.” They go out and buy, or lease, a new car, decide they want to buy a house, and get married.

Unfortunately, most federal student loan payments don’t usually kick in until December due to a six-month grace period after graduation. Be sure to check your loans…not all loans have this grace period.

If this OD has not understood what their monthly payment was going to be, and has already “maxed out” on a house and car, that doesn’t leave much room for personal savings or retirement planning.

PROJECT IMPACT OF TAXES

If our young OD is compensated as a 1099 IC (independent contractor) in a private practice setting, or has struck out on their own and opened their own practice, and has not done proper tax planning to withhold his tax liability that will come due in April, they will have an added hole to dig out of: not only will all of their current tax year liability be due, but they will also owe the first quarterly estimate for the next year.

The next 20 years (37 – 57)

FACTOR IN FAMILY EXPENSES

By this time, our optometrist has probably found a solid footing in both their personal and profession life. They’re married, have children, a mortgage, one or two car payments, and are probably still chiseling away at their education loans.

They now have to figure out a way to catch up for lost time on the retirement savings side of the equation, and also throw in college savings strategies for their kids because they don’t want their kids to be saddled with student loans like they are.

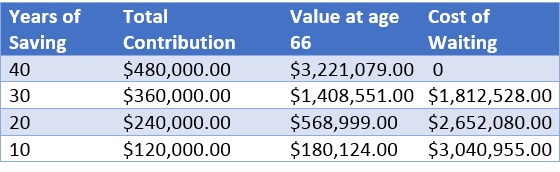

*See reference at end of article for further information about the two charts presented in this article.

DON’T COUNT ON SPOUSE’S SALARY FOR SAVINGS

The OD’s spouse’s income can help add to savings, but when you factor in child care, extracurricular activities, vacations, and other miscellaneous needs, this additional income often gets allocated to day-to-day expenses.

SET ASIDE FUNDS FOR PRACTICE INVESTMENT

If the OD is contemplating a change, or wants something bigger or better in their practice, they may not have the financial resources stockpiled to bridge the gaps in earnings, and cover the expenses, that usually come with practice expansion. They are forced to “take home” everything they make in their professional lives to underwrite their personal lives.

The Pinnacle (58 – 65+)

ADDRESS TIME CONSTRAINTS

At this point in our OD’s career, time and income are now usually working against them instead of in their favor.

ACKNOWLEDGE WHERE YOU STAND

It is typically around this age (55-60) that we sometimes have difficult conversations with ODs, and point out that the amount of money they’ve been able to save up to this point, combined with Social Security, and possibly even the sale of their practice, is not enough to sustain the quality of life in retirement that they’ve grown accustomed to living throughout their working career.

CONTINUE WORKING & CUT EXPENSES

Therefore, they have two options, and might have to do both, depending on how little has been saved: continue working past their desired age and/or take a potentially significant pay cut at the point of retirement.

Takeaway: At each stage of your career, stay aware of how much you have saved, after factoring in the expenses of your personal life, and create a plan to ensure you build the practice you envision, and avoid falling short at the age when you would like to retire. A good philosophy to engage is the following: Let your savings habits dictate your spending habits…not the other way around.

*The two charts presented in this article assume an 8 percent return and the reinvestment of all earnings. Return figures are for illustrative purposes only and do not represent the past or future performance of any actual investment, nor should they be used as investment advice. Example assumes investment is made at the end of each month and the reinvestment of all earnings, but does not take into account any applicable fees, expenses or any taxes.

Adam Cmejla, CFP®, is a Certified Financial Plannertm and president of Integrated Planning & Wealth Management, LLC, a financial planning and Registered Investment Advisory firm that works with optometrists nationwide. For more information: Contact Adam at 317-706-4748 or adam@integratedpwm.com.

Adam Cmejla, CFP®, is a Certified Financial Plannertm and president of Integrated Planning & Wealth Management, LLC, a financial planning and Registered Investment Advisory firm that works with optometrists nationwide. For more information: Contact Adam at 317-706-4748 or adam@integratedpwm.com.