By Ken Krivacic, OD, MBA

August 24, 2016

Practice owners are responsible for meeting multiple deadlines throughout the year. Some of the more important deadlines are those associated with making federal tax payments and filing the appropriate reports. We, as employers, must also provide employees and contractors with W-2 and 1099 reports. The rules can be overwhelming, and missing a payment, or making a late payment, can be costly to the practice, including penalties that come with fines.

The penalties for late payments are twofold. The first is a late filing fee which is 5 percent of the unpaid tax assessed every month until the tax is paid up to a 25 percent maximum. The second is a late payment penalty, which is 0.5 percent of the unpaid tax assessed every month until the tax is paid, again with a maximum of 25 percent.

You also can file for an extension and file your tax forms later. Our accountant invariably does this every year. That gives you more time to gather the information needed to file your taxes. The one thing it does not do is enable you to delay paying the taxes. You still must make an estimated tax payment on the required date. If the estimated payment is found to be short of what was required you will pay a penalty on the difference at the rates listed above.

To avoid financial penalties, it is essential to keep on top of all tax deadlines throughout the year.

In our practice, which has 21 employees, we use a payroll service for these duties. Early in my practice career I performed all these duties in-house. After several missed deadlines, and the consequential stiff penalties, we chose to outsource this function of the practice. Depending on the size of your payroll it may make sense to do payroll in-house.

In our office the average tax liability per month is close to $4,500. We pay the payroll service close to $250 per month to manage our payroll, including paying taxes. If we missed one payment the math tells us that it would be a wash. The service also offers us peace of mind as it is responsible for processing payroll and paying taxes on time.

You could use your CPA to help with tax filings, payments and deadlines, and ours helps us with those processes. However, most CPAs are not in the business of keeping up with every client’s month-to-month processes like a payroll service is. Again, if your tax liabilities are relatively low then it is a good way to go. Ultimately each practice, and consequently, each practice owner, is responsible for filing and paying their taxes on time. Whether you want to take care of that in-house, or farm that process out, is up to you as the practice leader.

However you decide to do it, you need to be aware of your responsibilities and the required filing dates.

Plan Ahead

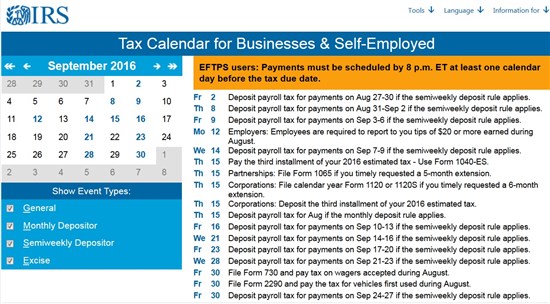

Tax planning resources, including calendars with due dates for each month of the year, are available on the Internal Revenue Service’s web site. Here is the calendar of important tax deadlines for small businesses, and the self-employed, for September.

Understand Basics of Tax System

If you employ even one person, the practice needs to obtain a federal employer identification number (EIN) from the IRS, if you don’t already have one for your practice. This EIN is used on all correspondence, deposits and returns.

In reporting, tax returns and tax deposits are generally done separately. Federal tax deposits must be made on a periodic basis and federal tax returns must be filed on a quarterly or annual basis. All tax deposits must be made electronically unless you have a federal tax liability of less than $2,500 per quarter, in which case you still have the option of mailing a check with your quarterly return.

Keep Track of Tax Due Dates

Due dates for employment taxes usually depend on the size of your employment tax liability. There are four possibilities:

Annually. If you have an employment tax liability that is less than $1,000 for an entire calendar year.

Quarterly. If your employment tax liability is less than $2,500 for the current, or preceding, quarter.

Monthly. If your employment tax liability is more than $2,500 for the last quarter and you reported $50,000 or less in taxes for the four quarter period ending on June 30 of the prior year.

Semi-weekly. If your employment tax liability is more than $2,500 for the last quarter and you reported $50,000 or more in taxes for the four quarter period ending on June 30 of the prior year.

Most of us in private practice will fall into the quarterly or monthly reporting category depending on the size of our practice. The taxes that need to be reported and deposited in the above categories are both Federal Income Taxes and Social Security (FICA).

Track All the Taxes You Are Liable For

As business owners, we are also responsible for Federal Unemployment Taxes (FUTA). These must be deposited on a quarterly basis unless your quarterly liability is less than $500. Once your FUTA liability exceeds $500 it then needs to be deposited at the end of that quarter. If your FUTA liability is more than $500, it must be deposited by the last day of the month that follows the end of each quarter. Those dates would be April 30, July 31, October 31 and January 31.

In addition, you are also responsible for filing returns that demonstrate how you arrived at the amount of the tax liability.

For Federal Income Taxes and FICA, Form 941 should be used and the deadline is the last day of the first month following the end of each quarter. Those dates would be April 30, July 31, October 31 and January 31.

For FUTA, Form 940 is used, and it is due January 31 following the end of the calendar year.

Provide Employees with Tax Materials

We must provide all employees who worked for us during the calendar year a W-2 form showing annual earnings, so that employees can file federal and state tax returns. The form must be distributed to employees by January 31 of the year following the calendar year covered by the form. You must also file copies of W-2s with the Social Security Administration by the end of February.

If you employed independent contractors in your practice they will receive a Form 1099 since you don’t withhold or pay any of their payroll taxes. You are required to provide this form to any contractor who received at least $600 in pay. The contractor needs to receive the form by January 31, and copies of the form must be sent to the IRS by February 28.

Maintain Tax Records

The final obligation we have as business owners is to maintain our tax records. For federal tax purposes, records must be kept for at least four years after the due date of the return, or the date the taxes were paid, whichever is later.

All these due dates and obligations can be overwhelming for a small business owner. If you are like me, and tried to do it on your own, and found it cost more in penalties due to missed deadlines, then I would highly recommend using a payroll service to administer this portion of your practice. The fee you pay for this service should more than make up for the time and headaches associated with managing your company’s payroll taxes.

Ken Krivacic, OD, is the owner of Las Colinas Vision Center in Irving, Texas. To contact him: kkrivacic@aol.com.